Written By: Veralynn Morris

FAFSA, financial aid, and divorce. These things are all considered complicated, and for good reason. So, when you mix them together, you get a whole lot of confusion.

Most people don’t want their kids to graduate college with mounds of student debt. Financial aid is the best way for students to get help paying for their degree. But financial aid isn’t straight forward and sometimes it doesn’t cover everything.

We talked about how divorcing couples can approach dividing their own student debt. How then, moving forward, should they approach paying for their child’s higher education?

So let’s take a look at the financial aid process. We’ll also look at some tips to help you get the most financial aid possible for your student.

FAFSA

The FAFSA, or Free Application for Federal Student Aid, is complicated even without separated or divorced parents. It is the most widely used application for colleges to calculate student financial aid packages. Then, depending on what information is provided, the student receives an aid offer from the institution.

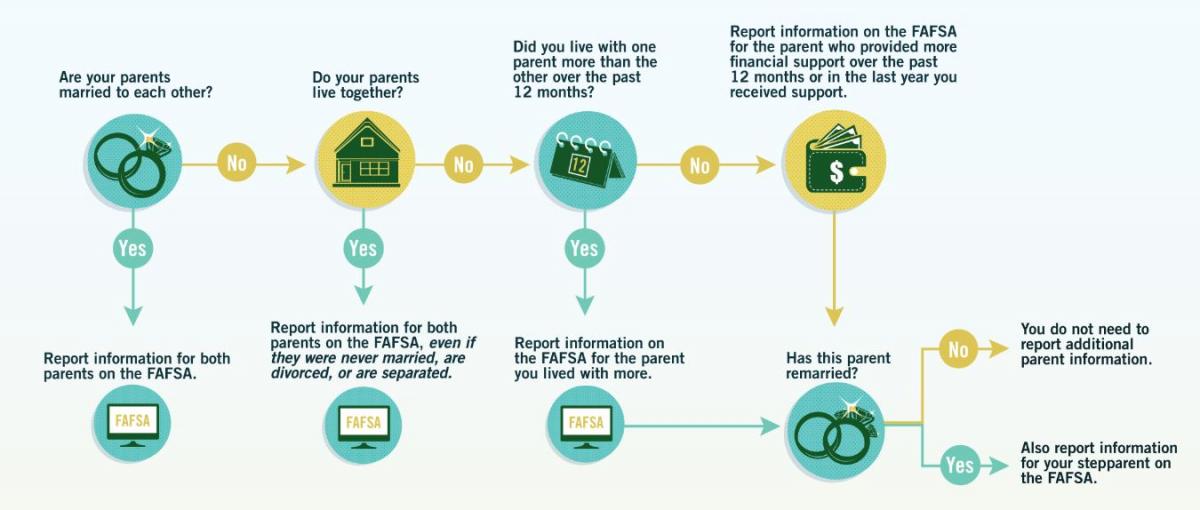

FAFSA defines marital status differently than the law does.

If a students’ parents live together in the same home, even if they’re legally separated or divorced, both parent’s information must be provided on the application.

If the parents are living separately and lead separate lives, even if they’re still legally married, they are not considered married according to FAFSA.

Who fills out the application if the parents are considered separate?

For FAFSA, it depends on which parent is considered the “custodial” parent. This term is defined as whichever parent the student lives with most of the time and who provides the most financial support. If both parents have 50/50 custodial privileges, then the student could list the parent with the lower income as the custodial parent. This would obtain the best financial aid. (Technically though, the child would have needed to live with that parent for one more day out of the year or receive more financial support for them to be considered the custodial parent.)

However, FAFSA also takes into consideration child support and alimony. Therefore, the lower income earning parent who receives funds in alimony and child support may not make the chances for aid any better.

FAFSA stipulates on it’s website that the parent who provides the most financial support within the last 12 months should be the parent listed on the application.

CSS/Financial Aid PROFILE

Some schools use a different formula to determine financial aid packages. At these institutions, the CSS PROFILE is used in addition to students filling out the information for FAFSA.

Unlike FAFSA, CSS requires background information for both parents regardless of marital status. The institutions that use this profile often believe it is important for both parents to be contributing to the child’s education. It is also a much lengthier application and allows for more special considerations.

By using CSS, it is argued that financial aid can be distributed more equitably. In comparison, FAFSA can sometimes give an advantage to students who do not have to list the non-custodial parent, even if that parent is contributing to their education.

Depending on your situation, it would be best to talk with the school’s office of financial aid. By doing so, you can learn more about how they calculate aid awards. This will also give you a better idea of what schools would give you and your student the best aid packages.

For more detailed descriptions of other divorce situations, consider reading this blog post from Mass Mutual. I’ve used it for reference while writing this article and it contains lots of information about specific cases that haven’t been discussed here.

Helpful Tips

The process of obtaining financial aid can feel very overwhelming, or unattainable. However, there are some tips that can help.

First, learn about the process well in advance. You reading this blog (and others) is a great start! It’s best to be informed and prepared rather than scrambling and losing out on aid later.

Second, make sure you apply! And apply early! Many students miss out on aid because they don’t think they’ll qualify. Others may miss out because some aid is first-come, first-serve. The opening date for FAFSA filing is October 1st. While the deadline of June 30th seems far away, it isn’t in your best interest to wait that long.

Third, if you’re getting divorced but aren’t yet, make sure your settlement includes how you’ll pay for college. Thinking about this early could put you in a better financial situation when the time comes.

Additionally, make sure that you know who the custodian and beneficiaries are on any 529 investment accounts. Which parent owns the account and which parent counts as the custodial parent can make a difference in the aid provided.

Finally, speak to an attorney who is familiar with these types of agreements. Also, talk with a financial advisor so you understand the consequences of various financial scenarios. With this information, you and your child can make a financially responsible decision as they pursue their degree.

Feel free to check out this site for additional information.